2023 is in the books and proved to be a resilient year as financial assets performed solidly in the end after climbing the proverbial wall of worry: a wave of bank failures in the US, recessionary fears, elevated inflation, continued tightening by central banks, political dysfunction in Washington DC, an earnings recession and a new war in the Middle East. However, US consumers remained resilient and in solid shape and proved once again they are the engine of US growth. While many economists expected a recession to hit at some point in 2023, the US economy actually expanded during each quarter of the year, with the latest official reading showing a robust increase of 3.3% year-over-year in the fourth quarter.

As financial conditions eased and the Fed signaled a potential shift to monetary easing in 2024, financial assets rallied in the fourth quarter to close out a year of solid returns. Domestic equities, as measured by the S&P 500 index, gained more than 11% in Q4 and 26% for the year as a whole. Interest rates came down across the board during the fourth quarter, fueling a bond rally as well. Corporate Bonds gained 8.5% while US Treasuries gained 5.7% in Q4.

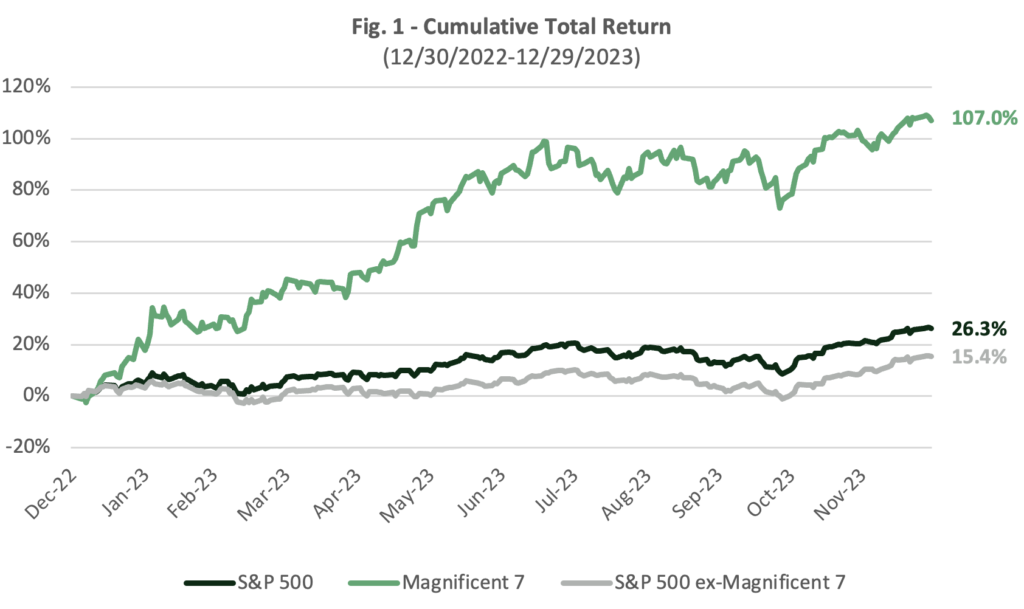

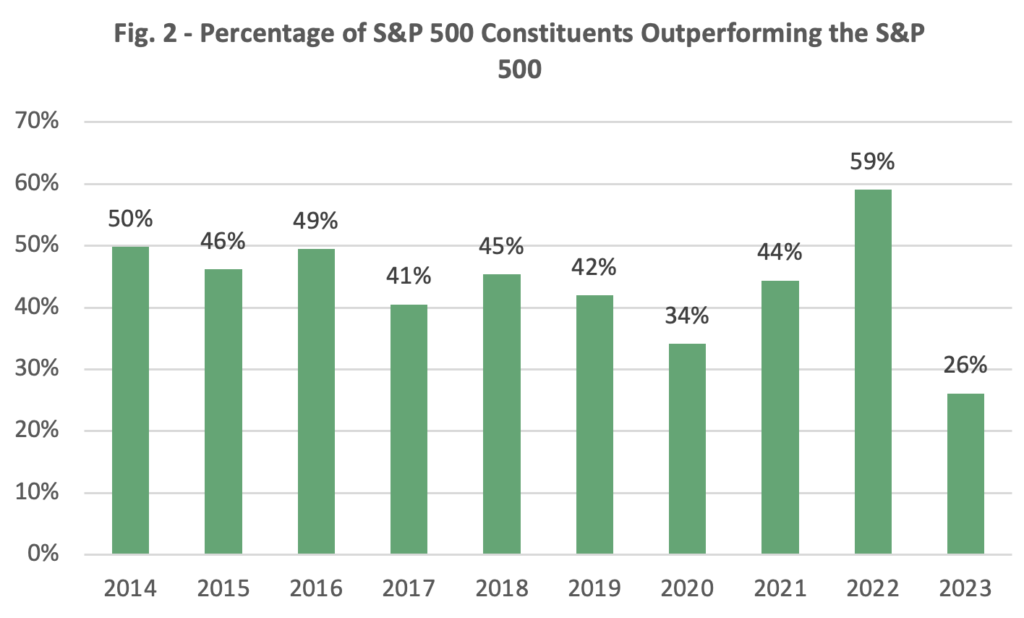

Regarding the US equity market however, the headline figure hides a disturbing picture under the surface. While the S&P 500 did rally by double digits for the 11th time in the past 15 years, market breadth was poor as the market return was driven by only a handful of stocks. Indeed, the Magnificent 7, as they have been called, are the seven largest US stocks by market capitalization (Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia and Tesla) and now represent almost 30% of the index. As a group, they gained 107% in 2023. Excluding them from the index, the “S&P 493” would have returned “only” 15.4% for the year (Fig. 1). The S&P 500 constituents’ median return was 9.7% and only about 26% of the S&P 500 constituents actually outperformed the broad market in 2023, which represents the smallest percentage in at least the past 10 years (Fig. 2).

Source: Bloomberg, Alpine Hill Advisors. Data presented on a total return basis (including reinvested dividends). The “Magnificent 7” is represented by the Bloomberg Magnificent 7 Index, an equal-dollar weighted equity benchmark, created by Bloomberg and consisting of a fixed basket of 7 companies (Alphabet, Amazon, Apple, Microsoft, Meta Platforms, Nvidia and Tesla). Investors cannot invest directly in an index.

Source: Bloomberg, Alpine Hill Advisors. The S&P 500 Index is represented by the SPDR S&P 500 ETF Trust.

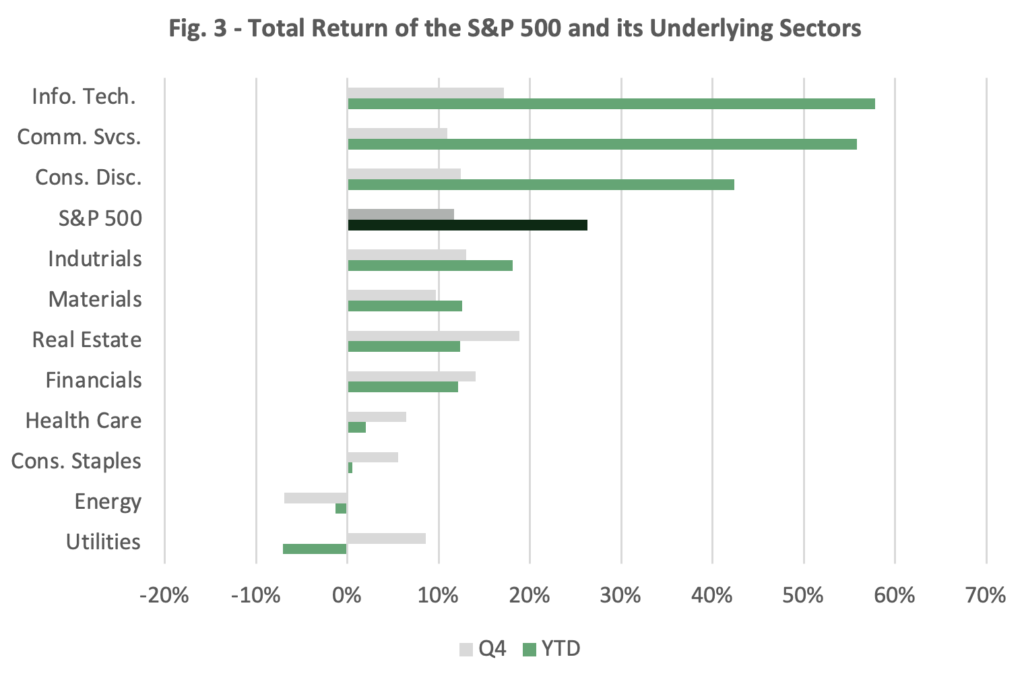

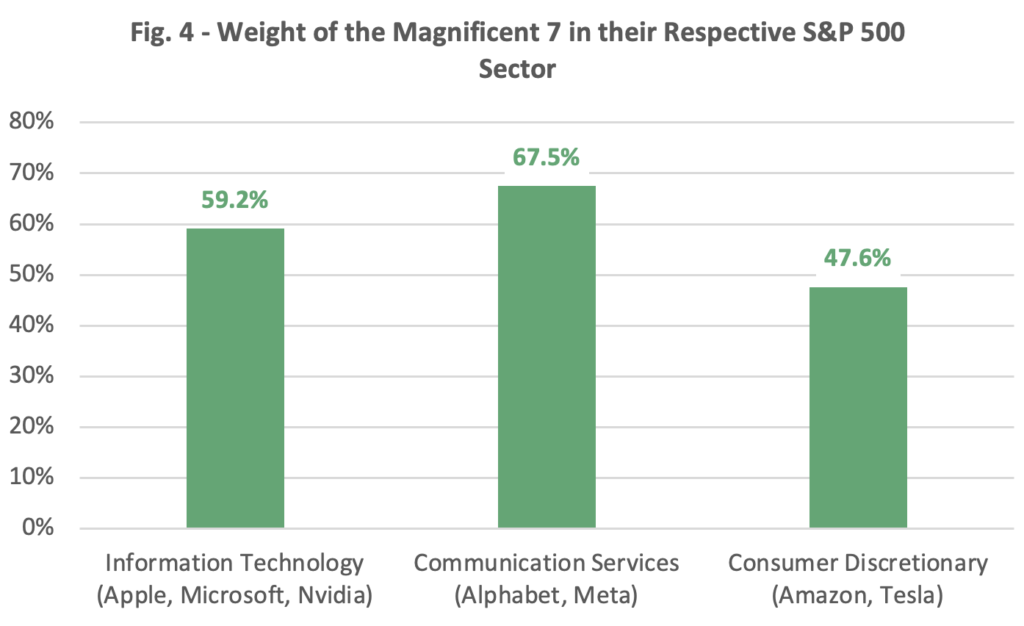

The same conclusion can be made by looking at sector returns (Fig. 3). While the S&P 500 gained 26% in 2023, only three sectors outperformed: Information Technology, Communication Services and Consumer Discretionary. All three are heavily influenced by members of the Magnificent 7 (Fig. 4).

Source: Bloomberg, Alpine Hill Advisors. The S&P 500 Index is represented by the SPDR S&P 500 ETF Trust.

Proponents of passive investing have long argued that one of the main benefits of being passive was to easily achieve diversification by buying baskets of securities. 2023 showed some of the limits of this argument. The “market” is now top-heavy, driven by a handful of stocks all sharing similar characteristics in terms of sector or style. Active managers who can be truly selective may be able to display their added value moving forward.

Markets begin 2024 with plenty of optimism and momentum. Financial conditions have improved, and the Fed has signaled a potential shift towards monetary easing in 2024. But we would caution that it feels like much of the good news is already priced in. While inflation has been reduced dramatically since the peak of 2022, it is still higher than the Fed’s target and may not reach that stated target without a greater economic slowdown. Market participants are expecting the Fed and other central banks to start slashing rates in 2024, but the pace and magnitude of the monetary easing remains uncertain. On the corporate front, profit margins have stabilized, and investors expect a double-digit rebound in earnings growth after a slight contraction in 2023, despite companies continuing to talk about a challenging macro environment during earnings season commentaries. All in all, we believe prudence may still be warranted as investors’ expectations are much higher in 2024 and may perhaps be too aggressive and complacent.

As a result, we continue to favor investing in high quality US equities, employing a barbell approach by focusing on long-term growth opportunities, especially within technology-focused leaders to capture AI-related tailwinds, coupled with more defensive, dividend-focused and/or lower volatility stocks to protect capital and smooth out returns in the short term. Similarly, within the fixed income space, we want to continue emphasizing stable income streams. After the Fed hiked rates 11 times between March 2022 and July 2023, the equity risk premium or attractiveness of equities versus bonds has dwindled and income has become easier to get by in general. While rates have generally come down in Q4, we have noted that yields on municipal bonds have declined by an average of about 32% across the curve during the quarter, a larger rate of change versus Treasuries and Corporates (Fig 5). As such, we continue to favor high-quality investment grade corporate bonds, especially for longer term investors, as well as short-term Treasuries for our cash and equivalents exposure.

Source: Bloomberg, Alpine Hill Advisors

If you have any questions or would like to discuss any part of my analysis, I would like to hear from you. Thank you for reading.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor Alpine Hill Advisors LLC (“Alpine Hill”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Alpine Hill and its representatives are properly licensed or exempt from licensure. Please visit our website https://alpinehilladvisors.com for important disclosures.